About Us

Badger Insurance Advisors is a Trusted Choice Insurance Agency, which means we are independent and are not confined to one specific insurance company. This matters because we work for you, not the insurance company! Risk is everywhere, let us help you protect your valuables: auto, home, or life insurance…whatever matters to you!

Contact Info

5916 N Lisbon St, Aurora, CO 80019

(8:00am - 6pm MST, Monday - Friday)

BY: KEVIN VOLZ | INSURANCE AGENCY PRINCIPAL

- PERSONAL INSURANCE

Why Should You Check Your Flood Zone?

Floods are one of the most devastating natural disasters. They can cause a lot of damage and loss to homes and property.

The last major flood to hit Colorado was September 2013. This storm produced widespread flooding from the Pikes Peak Region northward to the Wyoming border. Historic rains and flooding devastated 6 major rivers, 14 counties, and over a dozen cities and towns in Colorado!

The flood waters damaged nearly 19,000+ homes, 800 commercial buildings, 200 miles of roadway, and 20 state highway bridges. Total estimates for damage range from $1 to $2 billion dollars.

Wondering if you could be affected by a flood in Colorado, and how this will affect your flood insurance rates? Let's find out!

TIP

Your homeowners insurance typically does not cover damage caused by water that has come in contact with the ground outside.

Flood Zone Maps in Colorado

Luckily for you, there’s a convenient and FREE resource to figure out if your property, or any property for that matter, is located in a flood zone in Colorado!

The US Government provides flood maps online for anyone to review. Flood maps indicate which areas generally flood if water rises to a certain level.

These resources allow both personal homeowners and policy makers create more informed decisions about asset management, urban planning, and flood risk management.

How To Get Started?

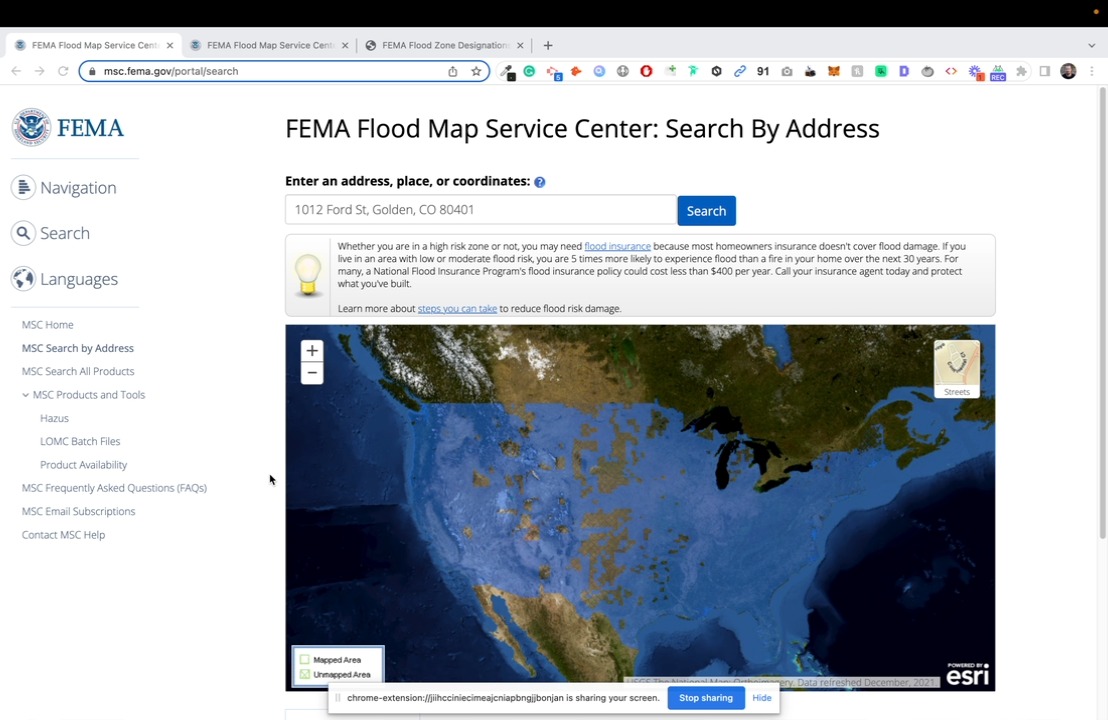

To get started, search for your home or specific property’s address on FEMA.gov and you’ll receive access to the nearest, most relevant flood map in that area. This can be exported through a PDF if you need to share this information with a loan officer, insurance agent, etc.

Note: If you’re working with a vacant lot that doesn’t have a registered address, try finding the nearest property that does have an address and search for that one

Here’s an example of what these flood maps look like:

This may be a bit intimating, and not as easy to digest as we teed it up to be, but it is!

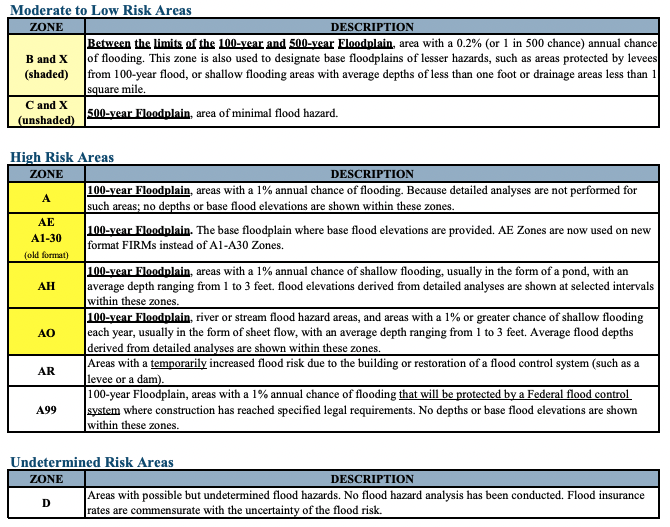

In this example, we can see that the pin in located in that orange section. From the table under the map, that the orange area indicates that the address is in Zone X , which is a 500-year Floodplain, area of minimal flood hazard, as known as a, Moderate to Low Risk Area. See the table below for a full definition of each flood zone.

If the pin was in the red/blue striped or blue area, that would mean the property would be in Zone AE, the base floodplain where base flood elevations are provided. AE Zones are now used on new

format FIRMs instead of A1-A30 Zones, as known as a High Risk Area. This is an area where flood insurance is high recommended or required.

How To Get Started?

So what if you're in a high-risk flood zone? What should you do?

If you’ve found out that your address is located in a flood zone, especially a high-risk flood zone, the first step is to contact a flood insurance agent in Colorado and verify whether your assumptions are correct.

They should be able to confirm or deny whether this is an issue and if so – how much it will cost you to insure over it.

BLOG AND NEWS

Better Insurance Decisions

Begin Here

READY TO GET STARTED

Get A Free Quote Today!

See how much you could save on your insurance with personalized quotes for Colorado residents.

or call us directly

Location: 5916 N Lisbon St, Aurora, CO 80019

Contact: (303) 359-1799 call or text

Time: (8am - 6pm MST, Monday - Friday)

Explore

Let's Connect